coding, and approval routing Automated data capture,

coding, and approval routing

with accounting systems Plug-and-play integrations

with accounting systems

supplier payments One-click global supplier

payments

POPULAR ARTICLES

- What are Duplicate Invoices, Why It Fails to Detect and How to Avoid It

- Financial Conferences 2023: Top US Finance Conferences You Shouldn’t Miss in 2023

- 10 Key Benefits of Accounts Payable Automation

- Spend Management: Definition, Benefits, Examples and Best Practices

- Accounts Payable Checklist: Everything You Need to Know

- AP Automation ROI: The Key to Streamlined Processes and Cost Savings

- AP Automation Vendors: A Complete Guide

- Invoice Automation: All You Need To Know For Your Business

- All About Invoice Matching: Streamlining Financial Processes for Efficiency

- 3-Way Matching in Accounts Payable: A Comprehensive Guide

- 2-Way Matching in Accounts Payable: A Comprehensive Guide

- 4-Way Matching in Accounts Payable: A Comprehensive Guide

- Accounts Payable Risk Assessment: How to Identify and Mitigate Risks

- General Ledger Code: A Complete Guide

- What is a TIN and How Does IRS TIN Matching Work?

Accounts Payable Journal Entry: A Complete Guide with Examples

Updated on: Nov 30th, 2023

|

13 min read

Financial data is generally structurally recorded in ledgers for storage. Accounts Payable journal entry is the method of recording payables data in the general ledger. Accounts payable are recorded in the balance sheet under current liabilities. So goods or services acquired under credit will be transacted against current liabilities. Recording financial transactions in the ledger helps in better budgeting and forecasting and aids your company's financial wellness.

Accounts Payable In Journal Entry

Accounts payable is the amount a business owes its vendors for goods or services purchased on credit. Accounts payable are generally settled according to a predetermined schedule agreed upon by the customer and the vendor. Hence, it is recorded as a current liability in the general ledger.

Upon purchase of goods from the vendor, the amount is recorded as a debit from the purchase account and credited to the AP account. When the payment is made to the vendor, the amount gets debited from the AP account and is credited to the vendor as cash.

Components Of Accounts Payable Journal Entry

A journal entry contains all details of a transaction made into or out of the company. The following information is generally recorded:

- Date of the transaction: The transaction date is recorded as the date on which the payment was processed to the vendor or when the goods or services were billed.

- The amount debited or credited: This contains details of the amount debited or credited to the account. Sometimes, the transactions can be marked as a debit against one account and credited to another within the same company.

- Transaction description: This contains a brief transaction description, including vendor names, payment terms, goods purchased, and invoice numbers.

- Account details: This contains the type of account the transactions are debited from or credited to.

- Expense accounts: This is the account dedicated to the type of expense or purchase made.

- Accounts Payable: This account is dedicated to all payments due to the company's creditors or vendors.

How To Record Accounts Payable Journal Entry

Accounts payable journal entry is recorded according to the type of transaction made. It can be recorded against a transaction from an expense account to your accounts payable charge.

Inventory or purchase

A purchase made for inventory or one-time purchases will be debited against the inventory or purchase accounts, respectively.

Damaged or undesirable purchase

In cases where damaged goods are returned to the vendor, the amount is either adjusted against the next purchase from the vendor or is credited to the buyer's accounts immediately. In this case, the money put on hold in the accounts payable account gets debited and credited back to the return account.

Purchase of assets

In cases where assets other than inventory purchases are made from a vendor, the amount is marked as a debit against the relevant asset’s account. It is credited to the accounts payable account.

Services purchased on credit

If the purchase made from the vendor is for a service, the expense will be debited against the relevant expenses account. If a department requires legal or consultancy services on credit from a vendor, this type of entry is added to the ledger.

Payment made to the vendor

When liability is paid off to the vendor, the amount is debited from the accounts payable account and is marked as credit into cash or the vendor’s bank account. The accounts payable liability then decreases for the company.

Processes Involved In Accounts Payable Journal Entry

The accounts payable process starts with the generation of a Purchase Order. A purchase order is a buyer's request for goods or services to the vendors. A liability, though, is only noted after the purchases have been delivered and an invoice is sent by the vendor.

Receiving invoices

An invoice is sent by the vendor after a purchase has been delivered. It contains an invoice number, amount to be paid, payment terms, due date, and delivery description. It is generally sent via mail or email.

Review the invoice

After an invoice has been received, it is generally reviewed by the accounts payable team for any discrepancies. This involves performing invoice matching, entering invoice details into the accounting system, and raising incorrect invoices back to the vendor. Implementing AP automation to automate the capture of invoice details aids this process.

Approve the invoice

After an invoice has been verified for errors, it is sent to relevant business heads for approval. This ensures that the services mentioned in the invoice have been agreed to and are payable to the vendor. If a bill is out of order, the business approver can reject the invoice, and the AP team raises the issue to the vendor.

Record the invoice

Once the payability of the invoice has been verified, it is recorded in the accounting system. All invoice details and when it is to be paid are noted down in the software and in the general ledger under accounts payable liability.

Pay the bill

After the invoice has been accounted for, it is paid to the vendor. At this point, the accounts payable liability is reduced, and the amount is credited to the vendor’s bank account via ACH, check, or wire transfer.

Example Of Accounts Payable Journal Entry

Example 1:

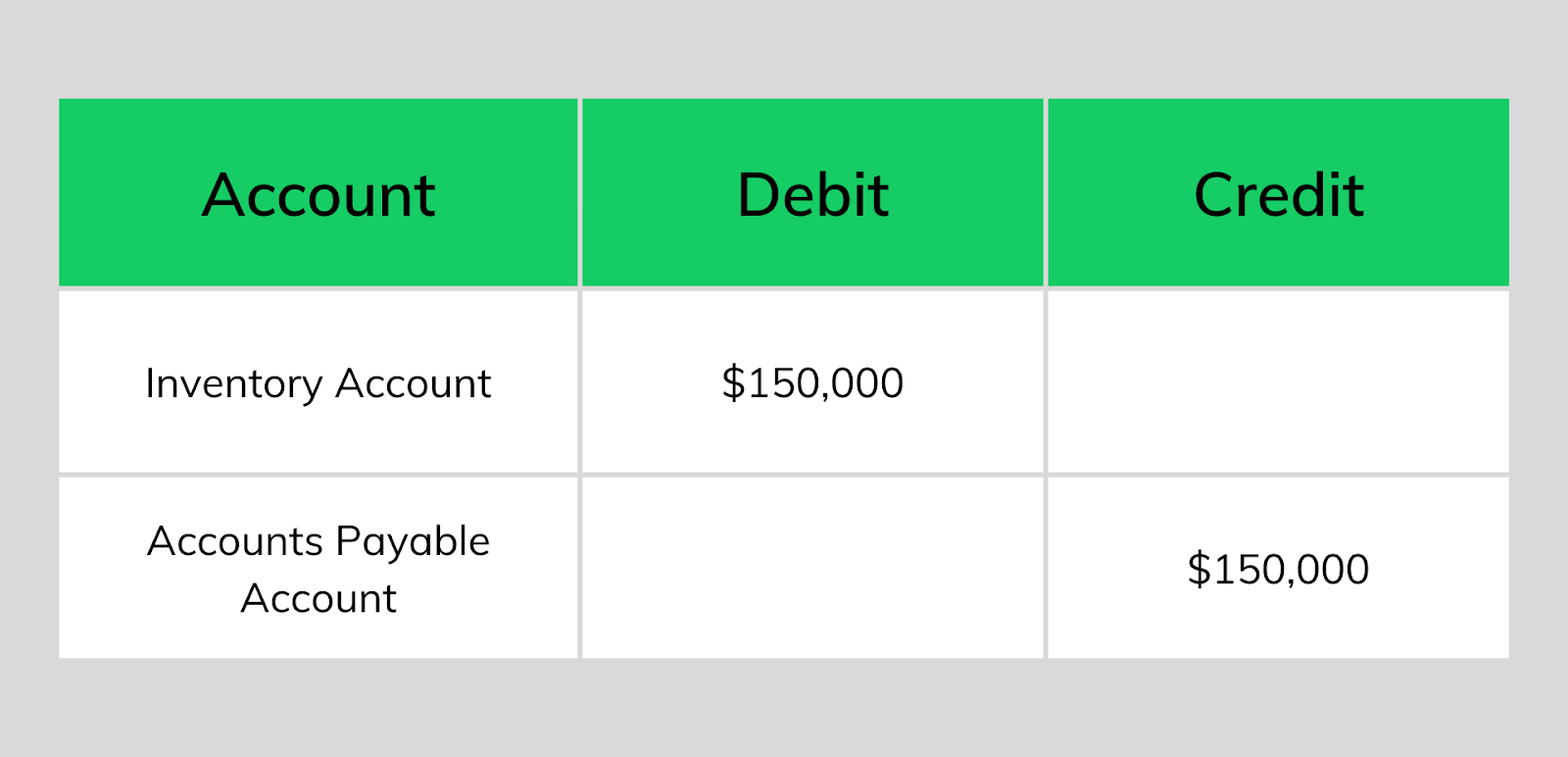

A furniture company purchased raw materials from a manufacturer on credit on 22nd August 2023. The company received an invoice from the manufacturer after the delivery of raw materials on 24th August 2023. The invoice states that the outstanding amount of $150,000 will be paid to the vendor before the due date of 1st September 2023.

Once the validity of the invoice is verified, the transaction is noted as follows:

After the bill has been paid, an opposite transaction for debit from the accounts payable account and credit into the vendor’s bank account is created as follows.

Example 2:

An IT firm purchases office supplies worth $20,000 from its vendor on credit on 20 August 2023 with Net30 payment terms. The firm notes down the journal entry for the transaction as follows:

After receiving the supplies, the firm realizes that $3,000 worth of supplies are not up to the quality standards. Since the vendor is not able to replace the products in time, the firm returns the products to the vendor and simultaneously decreases the accounts payable balance.

Once the vendor is paid back pertaining to the due dates a final journal entry is recorded for the transaction, debiting the entire amount from accounts payable account.

Automation In Accounts Payable Journal Entry

The accounts payable journal entry process is a largely hectic and ongoing one. Manually entering data into the ledger can leave room for manual errors, leading to missed transactions or invoices being paid twice. Enterprise Resource Planning software reduces the manual load of accounts payable journal entries by automatically accounting for expenses as soon as they are incurred. This ensures that you can account for your expenses even before paying them, avoiding any surprise costs. Some AP automation vendors, like ClearTech, automatically sync with accounting software and ERPs to account for an expense as soon as a bill is received. With line item level accounting in place, you can also account for an invoice in multiple cost centers and GL accounts.

Conclusion

Accounts Payable journal entry accounts for purchases made on credit under current liabilities. After debiting it from the relevant purchase or expense account, this is marked as a credit against the AP account. AP liability is reduced when a bill is paid against cash or vendor’s bank accounts. The accounts Payable process involves various steps, from receiving invoices, reviewing invoices, getting approvals, accounting for the invoices, and finally, the invoices get paid. Utilizing tools like AP automation software or ERP software can reduce the workload of manual journal entries from accountants and surprise costs by accounting for expenses accurately as soon as they are made.

Frequently Asked Questions