coding, and approval routing Automated data capture,

coding, and approval routing

with accounting systems Plug-and-play integrations

with accounting systems

supplier payments One-click global supplier

payments

POPULAR ARTICLES

- What are Duplicate Invoices, Why It Fails to Detect and How to Avoid It

- Financial Conferences 2023: Top US Finance Conferences You Shouldn’t Miss in 2023

- 10 Key Benefits of Accounts Payable Automation

- Spend Management: Definition, Benefits, Examples and Best Practices

- Accounts Payable Checklist: Everything You Need to Know

- AP Automation ROI: The Key to Streamlined Processes and Cost Savings

- AP Automation Vendors: A Complete Guide

- Invoice Automation: All You Need To Know For Your Business

- All About Invoice Matching: Streamlining Financial Processes for Efficiency

- 3-Way Matching in Accounts Payable: A Comprehensive Guide

- 2-Way Matching in Accounts Payable: A Comprehensive Guide

- 4-Way Matching in Accounts Payable: A Comprehensive Guide

- Accounts Payable Risk Assessment: How to Identify and Mitigate Risks

- General Ledger Code: A Complete Guide

- What is a TIN and How Does IRS TIN Matching Work?

Accounts Payable: A Debit or Credit?

Updated on: Oct 31st, 2023

|

11 min read

Accounts payable is purchasing goods and services from vendors on credit to be paid off later. Accounts payable, being a credit or a debit, is a common question, with the answer being - it depends.

All accounting transactions are noted in the general ledger as a journal entry. A journal entry keeps track of the flow of funds of the company. The transactions are noted as debit, i.e., money going out of the company, or credit, i.e., money coming into the company.

What Is Accounts Payable?

When a company purchases goods or services from a vendor as credit, it is called accounts payable. Accounts payable is a kind of short-term debt to be settled from somewhere ranging from a week to a month after receiving the invoice.

The accounts payable process starts by issuing a purchase order to the vendor requesting the purchase. The vendor supplies the deliverables and issues an invoice to the company, with payment terms as previously discussed. The company is responsible for paying the invoice on time or submitting any late payment fees. Since accounts payable are owed to the vendors, it is recorded in the balance sheet as a short-term liability.

Accounts Payable - A Credit Or A Debit?

Accounts payable are generally recorded in two kinds of transactions. When a purchase is made on credit, the transaction is debited from the relevant expense account but cannot be credited to the vendor, as the bill is paid later. To solve this problem, the amount is credited to the accounts payable account. In this case, accounts payable is noted as a credit.

Since accounts payable is a liability in the balance sheet, it is considered a credit.

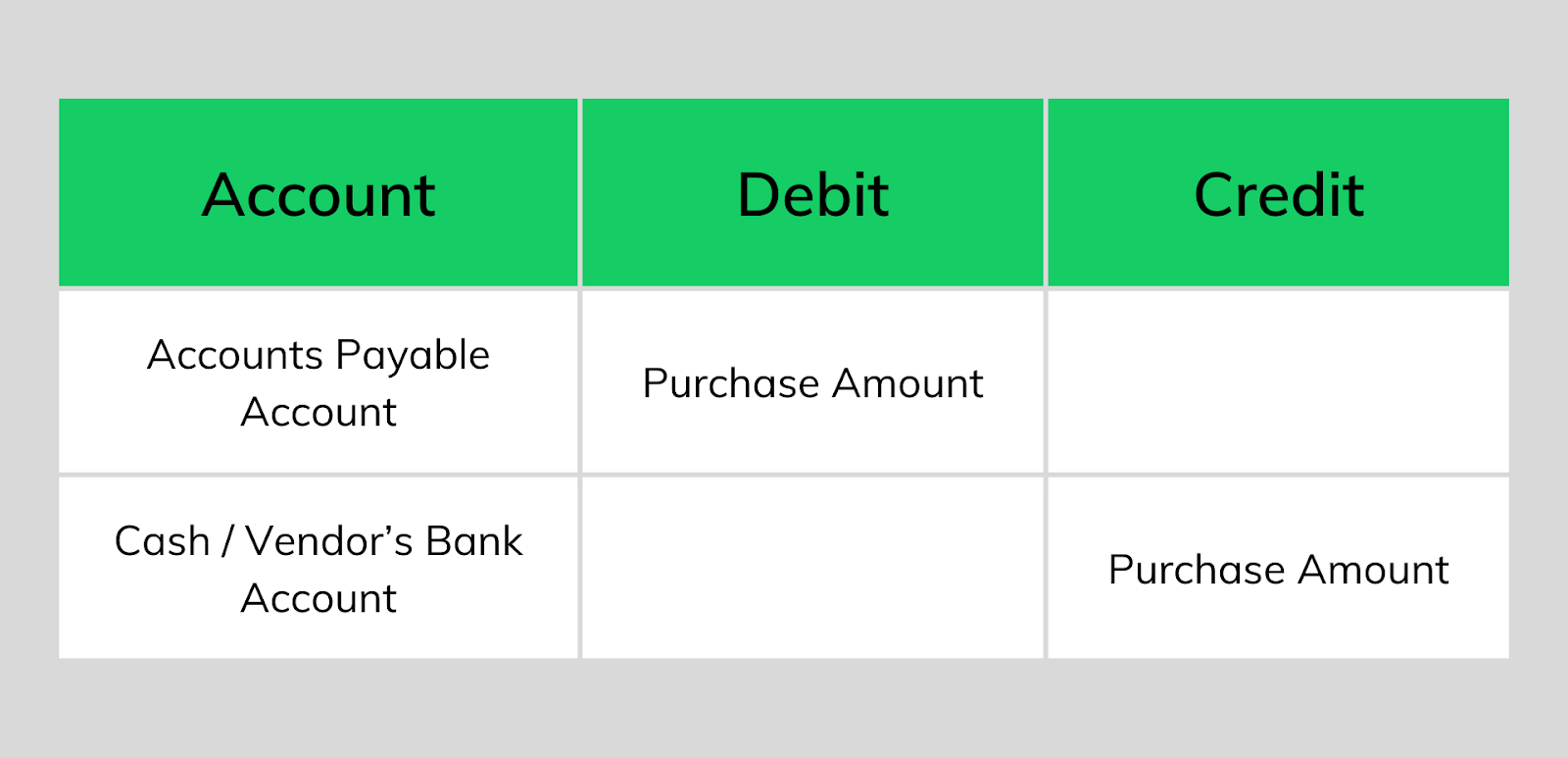

When the bill is paid to the vendor, the amount is debited from the accounts payable account and credited to cash or the vendor’s bank account to reduce liability. In this case, the amount is debited from accounts payable.

If products must be returned or discounted, the amount is adjusted in the next bill, thus decreasing the accounts payable liability. This amount is, therefore, debited from the accounts payable account and credited to the purchase returns account.

Recording Accounts Payable In Journal Entry

Accounts payable are recorded in the journal entry under credit when the purchase is made and under debit when the bill is paid.

When the purchase is made, the entry looks as follows:

After the payment is made to the vendor, the transaction is recorded in the general ledger as follows:

The accounts payable turnover ratio indicates how often a vendor is paid in a specific period. It is an essential metric for investors and creditors, as it speaks to a company's financial performance. The accounts payable turnover ratio requires accurate entry of all transactions made within the specified period. Maintaining correct journal entries makes calculating accounts payable while preparing a balance sheet easy. Having a view into all AP transactions will allow you to pay off debts timely, leading to a preferable turnover ratio.

Example Of Accounts Payable As Credit And Debit

Let’s discuss a few examples of accounts payable as a credit and as a debit:

Example 1

Suppose a car manufacturer operates in an office in San Francisco. The rent for the office space amounts to $10,000 per month, billed at the start of each month with Net 30 payment terms. After receiving the bill for August, the accountant creates a journal entry as follows:

The rent is paid to the vendor on 29th August in cash. After the rent is paid off, another journal entry is created as follows:

This reduces the amount in the accounts payable account, reducing the company's liability.

Example 2

Suppose the car manufacturing company purchases raw materials from its vendor monthly under Net 30 credit terms. The vendor provides the raw materials and notes the accounts payable transaction.

After receiving the material, the company discovers that some raw materials are of subpar quality. This material worth is returned to the vendor, and a journal entry is recorded.

After the vendor sends the updated invoice, the vendor is paid. The journal entry is as follows:

Automation In Accounts Payable

Recording a journal entry is very time-consuming and tedious when performed manually. Manual entry can lead to errors that harm the company’s financial health. Implementing accounts payable automation in your processes can reduce your accountants' manual load and payment errors. Automating your invoice digitization process also allows you to store all invoices on a single platform, making managing invoices easy. Many AP automation vendors, like ClearTech, sync all AP transactions back to your accounting system, creating a paper trail to aid in journal entries. Having complete visibility into your funds also allows you to maintain a good AP turnover ratio and improve creditworthiness. With ClearTech’s gated logins and smart spend insights into line item spikes and vendor spend trends, your company is safeguarded against invoice frauds and less prone to leakages.

Conclusion

Accounts payable can be considered a credit or a debit, depending on the transaction involved. Accounts payable is a short-term liability owed to a vendor for purchases made on credit. When the goods or services are confirmed or received, the amount is debited from the relevant expense account and debited into the accounts payable ledger. Upon payment of the corresponding invoice, the amount is debited from the accounts payable ledger and credited to the vendor in cash or directly to the bank account. In the case of returns, the amount is debited from the AP account and credited to the purchase returns account. Automation can make the journal entry process more manageable by automatically syncing all invoice and payment data to the accounting system.

FAQs

- Is accounts payable a credit entry?

Since accounts payable is a liability account, it is considered a credit account, where funds are credited after the purchase. However, money is debited from the accounts payable account when the vendor is repaid.

- What is the account payable journal entry?

Accounts payable journal entry refers to transactions recorded in the general ledger related to purchases made on credit. Accounts payable is a short-term debt, leading to both a credit and debit entry.

- What is accounts receivable debit or credit?

Accounts receivable are recorded as an asset in the balance sheet and are considered debit. However, when funds are received from the customer, they are marked against the account as a credit.

- Is credit payable or receivable?

Accounts payable indicates purchases made on credit owed to the creditor at a later date. Accounts receivable are goods supplied to a customer on credit, owed at a later date. Credit is payable at the end of decided terms.

- Are liabilities debit or credit?

In the balance sheet, liabilities are considered credit accounts, while assets are regarded as debit accounts.